- Bally’s Corporation has announced the terms of their acquisition of UK gaming technology platform provider Gamesys.

- Gamesys stockholders have the option of taking a cash buyout offer or the equivalent amount of Bally’s stock.

- Bally’s has made a number of acquisitions intended to bolster their position as an online sports betting operator.

More early week news from Bally’s Corporation (NYSE: BALY) addressed some of the specifics of their buyout of UK based technology provider Gamesys( LSE: GYS). Among Bally’s primary areas of focus since rebranding from Twin River Worldwide Holdings late last year has been to bring all of the technology resources they need under the same roof. They did this on the sportsbook side by acquiring highly regarded platform provider Bet.Works and adding several complimentary businesses including DFS startup Monkey Knife Fight and free-to-play specialist SportCaller. They hope to achieve a similar degree of synergy with their acquisition of Gamesys.

London traded Gamesys has built out a sizable portfolio of online casino and bingo brands including Virgin Games and Virgin Casino in the UK market, Tropicana Casino in New Jersey and other brands focused elsewhere internationally. With a growing number of US states expected to introduce online casino play in the years to come the idea is to leverage the Gamesys technology and expertise to quickly make Bally’s an industry leader. Or to quote the press release the combination of the two entities is “consistent with companies’ long-term growth strategies and positions Bally’s for sustained value creation”. Much of what was released is required under Rule 2.7 of the U.K. Takeover Code. If you want to take a deep dive into the deal you can do so with the archive of information on Bally’s corporate website:

GAMESYS DOCUMENTATION (BALLYS)

After an overview of financing specifics the press release offers this quote from Soo Kim, Chairman of Bally’s Corporation, hitting on the same topic of integration discussed above:

“We believe that this combination will mark a transformational step in our journey to become a leading integrated, omni-channel gaming company with a B2B2C business. We think that Gamesys’ proven technology platform alongside its highly respected and experienced management team, combined with the US market access that Bally’s provides, should allow the combined group to capitalize on the significant growth opportunities in the US sports betting and online markets. We are truly excited about the opportunities that this combination would offer and the enhanced and comprehensive experience and product offering that it would enable us to offer our customers.”

Neil Goulden, Chairman of Gamesys, offered his comments on the options that shareholders have for compensation:

“The combination would give unique optionality to Gamesys shareholders. The recommended cash offer, including the Gamesys FY20 dividend, provides a 41.2% premium to the Gamesys share price at the time of the original proposal from Bally’s and is at a significant premium to the all-time high Gamesys share price prior to the 2.4 announcement. However, should Gamesys shareholders wish to invest in a business with a strong foothold in the high-growth US gambling market combined with established markets in the UK and Japan, they can elect for part or all of their holding to be converted into Bally’s shares.”

The press release also gave this bit of synergistic analysis:

Bally’s and Gamesys’ boards of directors believe that the combination has a compelling strategic and financial rationale, would create long-term value for both companies and would be consistent with the companies’ respective long-term growth strategies. Gamesys would benefit from Bally’s fast-growing land-based and online platform in the United States, providing market access through Bally’s operations in key states as the nascent iGaming and sports betting opportunity develops in the US. In turn, Bally’s would benefit from Gamesys’ proven technology platform, expertise and highly respected and experienced management team across the online gaming field. The combined entity would be well positioned to capitalize on the full range of opportunities available both in the US and abroad.

Concurrent with all of this was an announcement from Bally’s that they will issue $600 million in common stock and $250 million of equity units with the proceeds earmarked to bankroll their acquisitions:

Bally’s Corporation today announced that it has commenced concurrent public offerings, subject to market and other conditions, of $600 million of its common stock and $250 million of its tangible equity units (“Units”). Bally’s intends to grant the underwriters in each of the offerings an option for a period of 30 days to purchase up to an additional 15% of common stock or Units, as applicable.

Bally’s expects to apply the net proceeds from the offerings to fund a portion of the cash consideration payable to shareholders of Gamesys Group plc (“Gamesys”) upon consummation of the previously announced combination of Bally’s and Gamesys (the “Combination”). If the Combination is not consummated, Bally’s expects to apply the net proceeds from the offerings for general corporate purposes, which may include repayment of debt, repurchases of its common stock, the redemption of the Units, capital expenditures, acquisitions and investments.

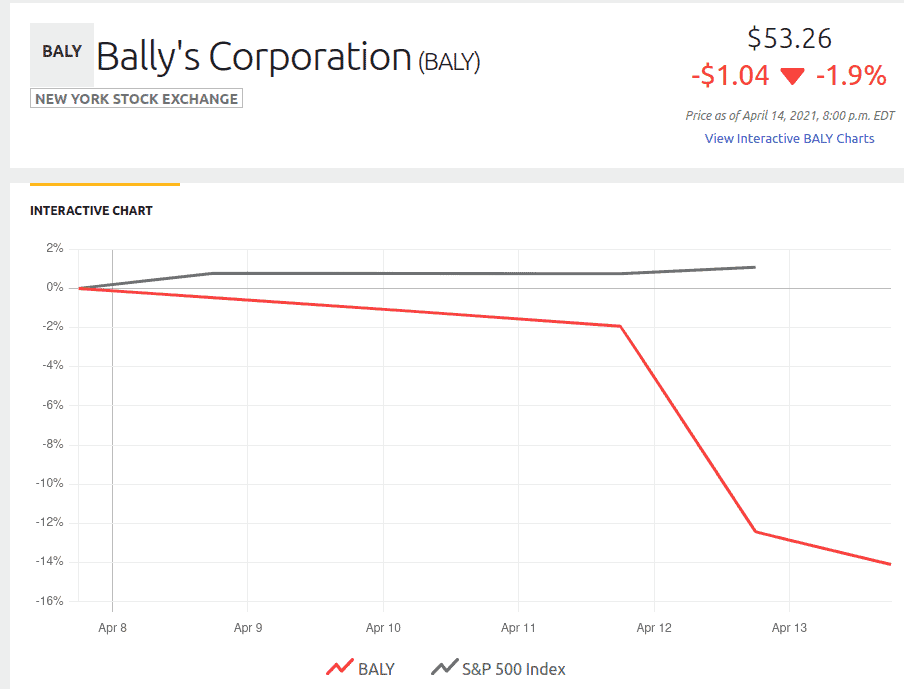

This was the news that went over like the proverbial ‘lead baloon’ with the US financial markets and players therein. Bally’s dropped four announcements on Thursday–the stock issuance, the Tropicana purchase, the Gamesys info and an earnings update for Q1. Simply put, there is much skepticism about the added dilution as a result of the $850 million USD of new offerings. Bally’s stock was up 8% for the year before Tuesday’s nosedive–it dropped as much as 15% intraday before closing off just under 11%. It dropped a bit more on Wednesday to finish at $53.26. Take a look at this ugly one week chart that I copped off The Motley Fool website:

Generally speaking, experts in the financial and gaming industries have taken a positive view of Bally’s strategic moves since the rebrand from Twin River Worldwide Holdings. Here at SPORTSINSIDER both myself and James Murphy hold Bally’s stock and generally love the company and the moves they’ve made to become a player in the US sports betting ecosystem. We don’t love everything they’ve done–both of us hated to see them getting involve in an overregulated and overtaxed mess of a casino project in Richmond, Virginia. It doesn’t look like a good fit relative to their other moves and if they want to expand their retail casino footprint there are much better opportunities to be found elsewhere. As if it weren’t enough of a potential grease fire they’ve now got local NIMBY’S expressing their opposition to the project.

Over on the financial side of the fence, the consensus view among analysts is that Bally’s stock is a buy/overweight/etc. Here’s a blurb that describes this sentiment and suggests that the heavy selling on Tuesday might have missed the forest for the trees:

On the same day, coincidentally, Bally’s reported solid preliminary quarterly results for the three months ended March 31, 2021. It expects consolidated revenues to be more than $185 million and adjusted EBITDA more than $50 million. KeyBanc’s analyst Brett Andress has reiterated an Overweight rating on the stock and raised the price target to $70, from $65, implying 10% upside potential. The analyst is betting on the reopening of Las Vegas to have a positive impact on Bally’s prospects. Overall, Wall Street rates BALY a Strong Buy based on 5 Buys. The average analyst price target of $77.60 implies 42.91% upside potential to current levels. Bally’s stock scores a 9 out of 10 on the TipRank’s Smart Score tool, implying that the stock has a strong chance of beating market expectations.

You can make a compelling case that Bally’s has done more to properly position themselves for the future of sports betting and online gaming than anyone including financial industry darling Penn National. Buying Bet.Works was genius, their deal with Sinclar Broadcasting to rebrand all of the former Fox Sports regionals was off the charts yet somehow still ‘under the radar’. By the end of 2021 they’re planning to launch mobile sports betting in the four states that are arguably doing it better than anyone else: Colorado, Indiana, Iowa and New Jersey. As long as they don’t get bogged down with that Richmond casino mess the sky is the limit for Bally’s based on sports betting/online gaming alone.

At the time of publication, Ross Everett has a long position in BALY.